The World Breeding Federation for Sport Horses is a forum where member associations raise concerns and share common interests. A recurring theme has been the uncertainty of this industry’s future. This uncertainty is exacerbated by the lack of information on the present. In response to this deficit we have elected to prepare a State of the Industry report.

The idea is to create a snapshot of the scale and activity in Warmblood breeding and to place that in the context of the horse industry and agriculture in general.

This information is intended to complement other efforts (for example the green initiative) rather than duplicate them. We hope to provide a reference point in 2020 and future reports will use that as a reference.

Jan Pedersen – President, WBFSH

The Sport Horse Industry 2021: Laying the groundwork

Preface

This Report was conceived to provide those involved in the horse industry with a snapshot of the recent past. In so doing the authors had hoped to identify sources of information that would inform business decisions and government regulations. We discovered that information is siloed within the various sub-sectors and that almost no effort is made to develop a big picture. We also discovered that the organizations currently serving horse sport and sport-horse breeding cannot respond to information requests. It is worth mentioning that the FEI is a notable exception. They routinely publish and make available activity based information, they also track ownership and ridership, reflecting their operations in all corners of the world. In sharp contrast, repeated information requests to National Federations and most WBFSH studbooks were ignored. As a result, the breeding information we have gathered is sparse and summative.

Despite this an effort was made to describe the industry’s scope and open discussion on some of the headwinds that impact growth. Given the resources available this report is necessarily descriptive rather than analytical. Collecting and reporting this information annually may identify trends and opportunities to help sustain the industry, improve the welfare of the horse, and ensure future generations can continue to enjoy the benefits of an ongoing relationship with these amazing animals.

1. Introduction

Humans have long been inextricably linked with horses. It is no surprise, therefore, that as mundane usage has waned, the sporting aspect of the horse has grown from friendly competitions between cavalry officers to international prominence and Olympic fame.

The Sport Horse Industry is multifaceted and even the definition for ‘sport horse’ has multiple interpretations. While there are many sporting aspects to how horses are used, we define sport horses as those bred primarily to compete in jumping, dressage, and three-day event, and secondarily in hunter and marathon-driving competitions. The main breed for an Olympic horse is the Warmblood. This animal is indigenous to Western Europe and its modern presentation has been developed from the farm/military horse of the 17th century. The first studbook was the Hanoverian, established late in the 19th century. Today most European states have at least one Warmblood studbook. Outside Europe breeding programs are often based on imported stock and are overseen by a national or, in some cases, a European-daughter studbook. Anglo-Arabian horses are also bred for sport while other breeds such as Thoroughbreds, Friesians, Lusitanos, and Pure-bred Spanish horses are also used, although not bred primarily for the FEI sport disciplines.

Beyond the agricultural breeding base, due to the widespread popularity of Olympic equestrian sports, the industry encompasses economic activity in farming, manufacturing, transportation and entertainment, and media. The sport and recreation activities themselves involve coaching, training, health, and other social benefits. In this report we hope to capture some of these activities. However, from a practical perspective and, while keeping the larger picture in mind, this inaugural report will focus on three areas: 1. analysis of the breeding, marketing, and sport portions of the industry; 2. regulations and regulatory bodies, and 3. issues and trends facing the industry.

2. Objectives

The research for this report was undertaken to provide breed associations, sport organizations, and regulatory bodies a high-level perspective on the sport horse industry. Of course, the report is primarily targeted to individuals and organizations outside the horse industry. The questions investigated are those which have been raised in various fora, supplemented with geographic and demographic information. Our member organization (the WBFSH) may use this information in developing programs that will help breeders understand the marketplace.

This Federation intends to use the report process not only to monitor the status quo, but also to identify emerging challenges. It is for this reason that the reports will include information on non-Warmblood breeds, transport and health, and demographics.

3. Sources of information, methods of collection, definitions

There were four main sources of information:

1. Registration information collected each year from our member associations;

2. FEI data on usage and geographic distribution;

3. Survey information collected in 2021 spring and summer by Carolin Kathmann, Nadine Brandtner and Ana Filipe;

4. Online reports researched and assembled by the report team.

It should be noted that none of the sources may be considered peer reviewed, auditable, or otherwise independently verified. Having said that, it is assumed that the data collected fairly addresses the questions. Online documents included reports from other organizations; often the financial sections of these reports include verification by independent audit.

We encountered several problems with data collection. The comprehensive survey was sent out rather late and as a result the response rate was very poor. In addition, we determined that the survey tool itself created problems in that a survey had to be completed in a single sitting. This and other small technical issues will be corrected for subsequent editions. Surveys conducted by Kathmann and Brandtner were better received and we are grateful that the results in part may be shared here.

4. Warmblood profile – breeding and usage statistics by region

4a. Warmblood production.

Without a doubt most Warmblood horses are produced in Europe, and in particular Western Europe. Considering that these countries have practiced economic cooperation for many years, it is not surprising that studbook structure and breeding practices are very similar among this group. Having said, that there are some notable exceptions. The primary studbook of Eire continues to include, although in minor part, traditional sport horse breeding practices where Thoroughbred horses are crossed with native cold blood breeds. Despite this and other similar examples, Eire and most European countries primarily use outcrossing as a refining option and their studbooks generally feature Warmblood by Warmblood crosses. As may be deduced, Warmblood sport horse books may be described as ‘open’; that is, defined outcrossing is permitted. The Trakehner sport horse is a notable exception; its breeding book is ‘closed’.

4b. Studbooks- how many are there?

Many warmblood horses are registered in studbooks that fall under national or regional government regulations. The WBFSH has 79 member studbooks representing the vast majority of the known Warmblood production. These regulations are intended to protect the intellectual property engendered in registration, and support the breeding principles espoused by the registry. But, it is not possible to determine how many Warmblood registries exist. In some countries registries operate as private businesses. These registries typically mimic the requirements of larger studbooks. The overall production they represent is unknown.

4c. Warmbloods – how many and where?

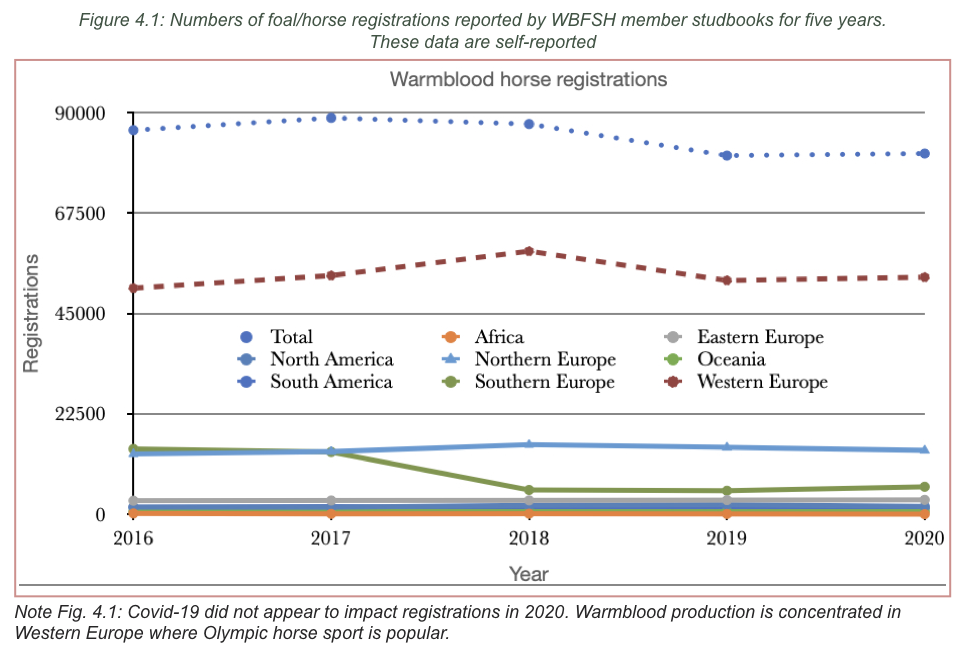

WBFSH data indicate that the majority of warmblood horses are produced in Europe (Fig. 4.1), and primarily in Western Europe. We emphasize that this data is based on membership reports to the WBFSH.

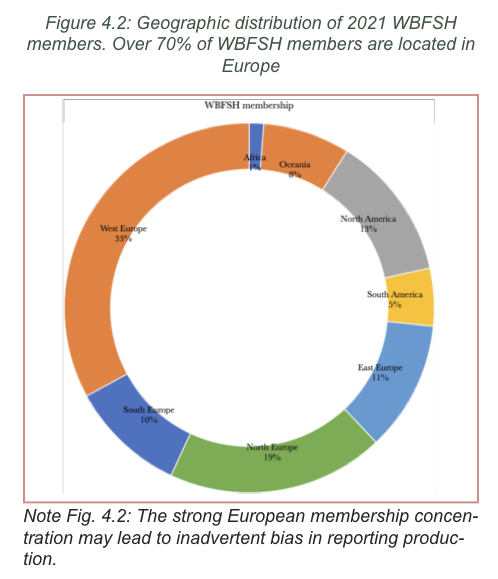

Figure 4.2 shows the distribution of member studbooks in the same geographic regions. Membership is dominated by European studbooks. It is difficult to accept that North America with in excess of five million horses and an estimated 28 billion dollar horse industry produces so few (1,500-2,000 per year) Warmblood horses each year.

4d. Sport usage

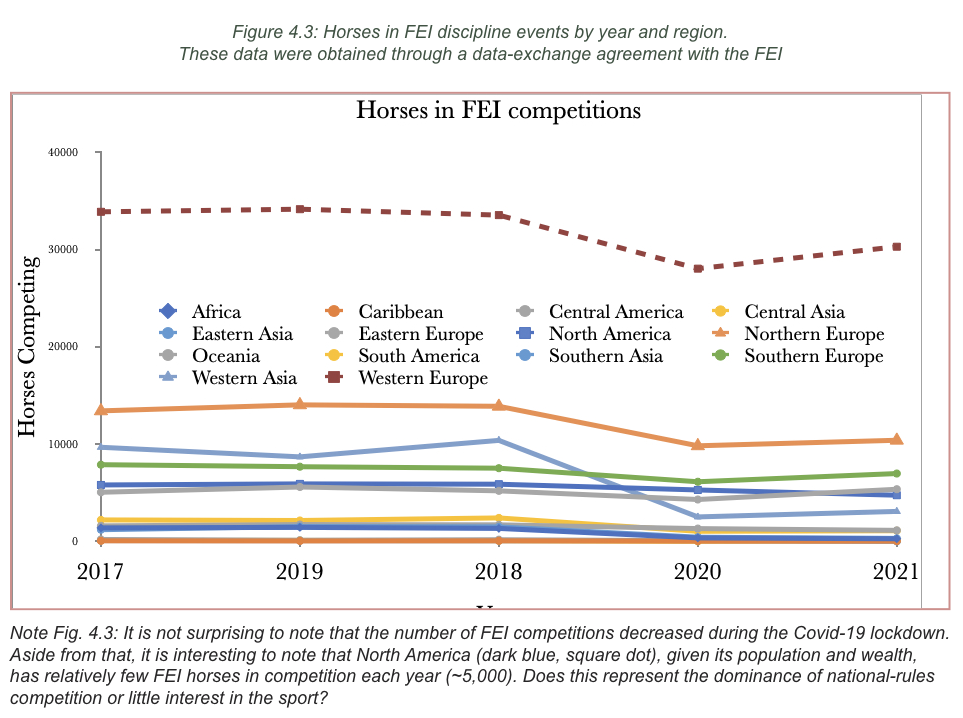

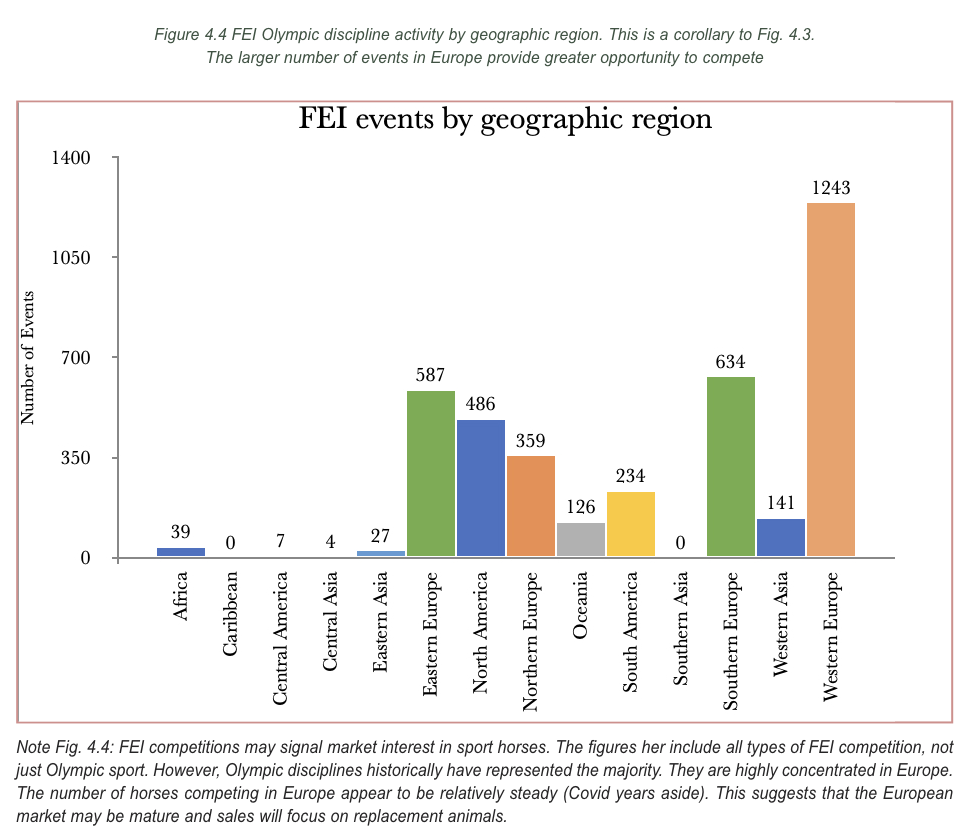

The data for this section shows the number of horses competing in FEI disciplines (Fig. 4.3) and the number of FEI competitions (all types, Fig. 4.4) by geographic region. The greatest number of horses and events occur in Western Europe. The participation rate in Europe and western Asia is low to high 20s per competition. Much of the rest of the world is below 10 FEI horses per competition. Since the FEI provides the most standardized competition, the high participation rate in Europe is understandable since one does not have to be aware of the variations in national competitions. It also suggests that the higher level of competition represented by FEI competition is more accessible in Europe than in other regions.

4e. Sport disciplines

The FEI data provided a breakout on participation by Olympic discipline. In Figure 4.5 the number of horses and riders are shown for Dressage and show jumping. Participation in the latter discipline far exceeds that of dressage. There may be a couple of contributing factors. First, note that the ratio of dressage horses to riders is approximately 1. This means in order to increase horse participation it is necessary to also train a rider. On the other hand, in show jumping each rider has four horses, meaning that training one show jumper creates a market for four horses.

Why does the discrepancy in horse-rider ratio exist? One may speculate that the highly structured dressage competitions necessarily limit the number of participants that can be judged in a day. A second factor is that prize money in dressage is very low or non-existent. In contrast, the show jumper has an expectation that a winning ride will realize a reasonable purse.

4f. Implications for breeders

Although the expense of raising sport-horses varies by region, there is no region that is truly low-cost. In those regions where there is little participation in premier level sport, it clearly makes more sense to purchase a competition animal than to attempt to breed such an animal. This may have created a knowledge gap where existing horse producers are unaware of a potential market or do not understand how to adjust their production model to address that market. Moreover, organizers are likely to host events with local rules such as gymkhana, hunter or trail disciplines. These events are suited to indigenous horses and less so to warmblood horses.

For additional information on the differences between Hunter and Jumper competitions in the North American market, the reader is referred to:

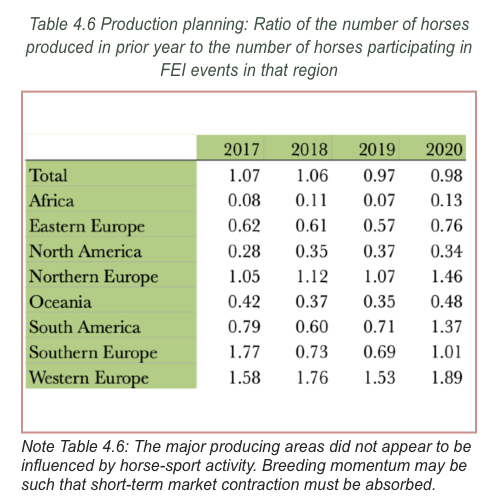

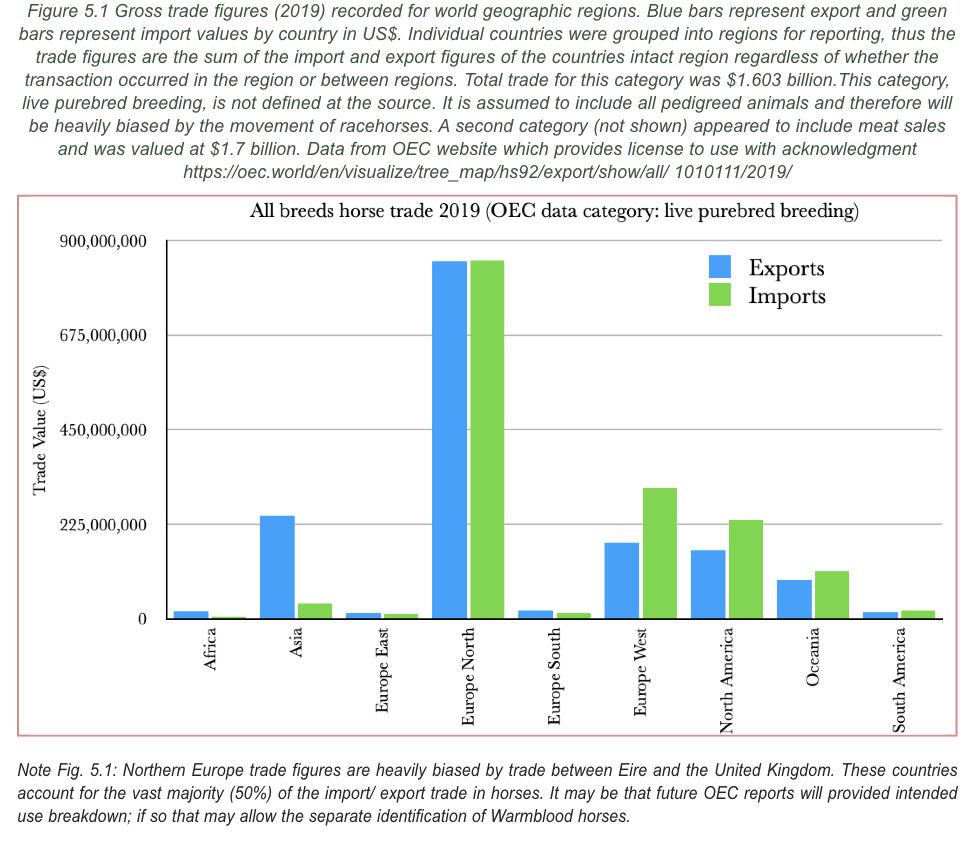

Of course a question in everyone’s mind is how well we are matching supply and demand, since that in turn will determine how well prices hold up. We do not have all the regions represented in the WBFSH membership, so Asia, the Caribbean and some of the Americas are not included. What information we do have suggests supply matched demand quite well until the pandemic when the number of events plummeted. What we also have is a strong indication that Western Europe consistently is producing far more horses than are used in the home market, and so must export them to other regions. OEC data, presented below, points to the USA as a major horse importer.

6. Sales activity

We have a little information on Warmblood sales thanks to our collaboration with World Breeding News. Although many Warmblood horses are sold at auction, it is unlikely that this represent the majority. There are more than 80,000 sport horses foaled each year, the vast majority in Europe. The auction sales data we have account for just over 6,000 horses, less than 10% of production. This is an important gap in our information since an active marketplace suggests growth potential, whereas a slow market may warn breeders to trim production. Given this. it would be instructive to know how many transactions occur in a year, not just those that occur at public auctions.

It may be possible to infer transactions from ownership changes recorded in studbooks (required now for traceability). That information will not include the purchase price and so cannot contribute to market value information.

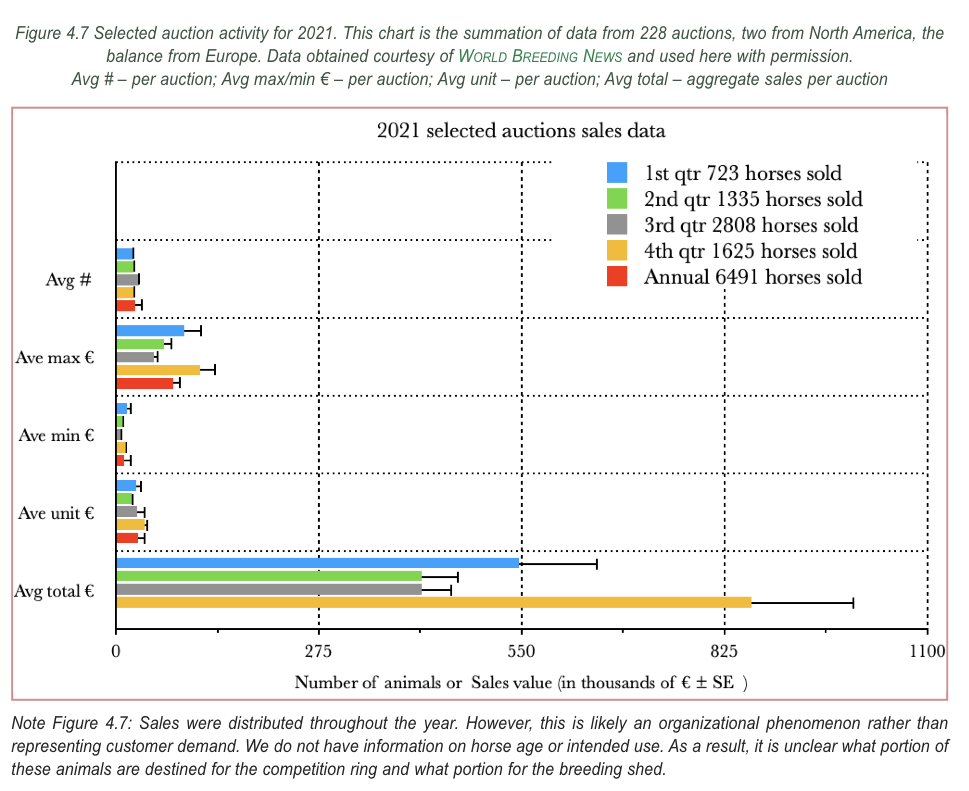

Figure 4.6 presents what data might be included in this report using partial results of auction activity obtained from our partner World Breeding News. A total of 228 auction results were reported for 2021, representing 6,491 sales. The auctions reported maximum and average sale price. They, primarily but not exclusively, were hosted in Europe. We have no information on the origins of buyers. It is also worth mentioning that we do not know if auction sale prices are similar to private sale prices. There are indications that auctions represent a small fraction of the total market.

7. Warmblood trade: international

Horse trading is a time honoured endeavour, its current form retains many historic practices while adapting quickly to new technological developments. Horse trade has a high economic multiplier effect due to the longevity of usage and the added value that takes place through rearing, training, showing and reselling. As a consequence, the value chain tends to be much longer than for other agricultural products.

7a. Establishing Value

The focus of sport horse breeders is on producing the best horse suitable for specific equestrian sports. Due to the popularity of equestrian sports and the range of competitive levels from elite international competition to lower level amateur sport there is a huge discrepancy in value between animals. Recreation and lower level competition horses are found for a few thousand while elite athletes at the peak of their performance are valued in excess of millions. In simple terms, value is determined by risk or probability. Purchasing a foal comes with high risk or lower probability that it will ultimately perform at the highest level, therefore lower cost, while a mature horse already trained and performing at a high level is a low risk investment relative to the desired performance, consequently demands a much higher market value.

7b Business Models

There are four basic business models:

1. Breeding and selling foals within the first year often amateur or part time breeders. This is the predominant model exercised in the racing industry. It has merit in sport-horse production in that it allows a breeder to focus on production, a skill set very distinct from training and showing.

2. Breeding and producing young trained horses. Breeders may have entered horse production to support family members or having retired from active competition. They have onboard training skills that can be used to increase the relative value of the animals they produce. However, this activity comes with the risk of injury to the horse (or no talent!).

3. Breeding and buying young horses to rear, train and sell often on a large professional scale. This is a model popular in Europe where the market is fairly dense. Many horses are available as are many skilled riders. This is also practiced in North America, although less often.

4. Buying horses to develop and sell in sport. (dealers and trainers). Again this is a popular model in Europe and removes the risk of losses during the production phase. It does retain the risk of loss during training and may not guarantee access to the best horses.

These business models address both domestic and international trade. Domestically bred sport horses make up the bulk of the horses used in the major producing areas, while imported horses predominate in areas with little or no production capacity. Consequently the high producing areas take up most of the export international trade. The EU is a common market so trade and movement of horses between countries is largely unfettered. As the largest producing and using area it is clearly the area where trade in sport horses is most intense.

7c. International trade barrier

Aside from the onus of completing forms and maintain identity paperwork, the primary barrier to international trade is health regulation requirements. The rules governing the importation or exportation of equidae are dependent on the National Veterinary Authorities of both the importing and, to a much lesser extent, the exporting countries. Entry of equine animals in the importing country is granted based on freedom from disease and an international health certificate is required for this purpose. Equidae are categorized by intention, namely equine animals not intended for slaughter, equine animals intended for slaughter and registered equine animals. Each animal must be correctly identified for effective disease surveillance and traceability. Horses are considered the most mobile segment of livestock worldwide, and the occurrence of equine infectious diseases would greatly compromise production and equestrian sports development, as well as equidae movement between countries.

The World Organization for Animal Health (OIE) provides guidance to National Veterinary Authorities worldwide, having elaborated a list of obligatory notifiable diseases in equine animals, which includes the following: Virological diseases:

• African Horse Sickness (AHS)

• Eastern, Western and Venezuelan Equine encephalomyelitis (EEE, WEE, VEE)

• Equine infectious anemia (EIA)

• Equine influenza (EI) and Equine Viral Arteritis (EVA)

Bacteriological diseases:

• Contagious equine metritis (CEM)

• Glanders

Parasitological diseases

• Dourine

• Equine Piroplasmosis (EP).

Further information about the OIE notifiable diseases can be consulted in the OIE Terrestrial Manual and Terrestrial Code. In the Terrestrial Manual, the OIE also offers recommendations on ideal diagnostic testing methods and vaccination protocols.

For some of the OIE listed diseases, there is an increased risk of transmission, even when standard health conditions and biosecurity measures are observed. To mitigate this risk, specific health requirements are established. For example, the prevention and control of Equine Influenza and Equine Encephalomyelitis relies on the use of vaccines. A vaccine is therefore required depending on the disease status of the exporting country. For breeding animals, infection with Taylorella equigenitalis (Contagious Equine Metritis) is detrimental, and with most animals being asymptomatic carriers, a negative CEM test is required during the 30 days prior to shipment in some countries. In the absence of an effective vaccine against the disease, negative diagnostic tests for Equine Piroplasmosis and Equine Infectious Anemia are also required. For equine piroplasmosis, it is mandatory to test animals before they travel to establish their serological status. Depending on the importing country, a quarantine period may also be necessary for optimal disease control.

Where the health status for a particular disease or diseases of two countries is not congruent, trade may be impeded bilaterally or unilaterally. Temporary regional outbreaks will similarly impact free trade. EU countries have a high volume of animal trade and consequently have a robust animal health reporting and tracing systems for all animals including the equidae.

This is not the case in countries and regions that do not rely on international trade to meet domestic demand where traceability more or less originates at the processing facility. Finally, there are countries such as Canada and the United States that have animal disease tracing for species primarily involved in food production but do not include equidae.

So three primary health issues affect trade in sport horses:

1. Disease status of import and export countries.

2. Regional or temporary disease outbreaks

3. Ability to track and control foreign animal disease The questions regarding international trade that require examination are:

1. Do any of these diseases that limit trade constitute an artificial barrier or are they all justifiable for economic and sanitary reasons?

2. Which areas of potential growth for the industry are negatively affected and what can be done to correct the situation?

Thoroughbred horses are used in Warmblood breeding programs and attract considerable attention through racing. By far the greatest users of Thoroughbreds are Eire and the UK. The Jockey Club reports just under 7,000 foals are born each year. The UK and Eire produce around 13,500 foals each year. It is fair to note that Thoroughbred production enjoyed an upswing from 2012 to 2017, but appears to be tapering off since then.

8b. Quarter horses

Quarter horses are not used in Warmblood breeding programs, but they do compete for the horse-interested set. Quarter horse breeding and activity are tracked by the American Quarter Horse Association. They report 81,213 new registrations for 2020 and 59,655 new registrations for 2019. They also track the horse population as births over deaths and indicate that the QH population is over 2.8 million worldwide. The vast majority of these animals are in the USA.

This highly centralized organization has made significant changes in recent years to attract young people to their sport and lifestyle. Despite this, membership has declined from a high of 353,000 in 2004 to 226,577 in 2020. There is no doubt that the North American demographic is contributing significantly to this decline. The AQHA track title transfers as an indicator of sales activity. They report 106,864 transfers for 2020. This does represent a good sales volume from a base of two million animals. The AQHA approves many events for Quarter Horses. They report 1,196 shows for 2020 with an average entry of 300 horses and 484 riders horses per show. Typically this organization approves about 2,500 shows per year.

Marco Ricotta (ITA) riding Peppy Secolo, World Equestrian Games, Aachen, 31 August 2006, Reining Team and Individual qualification

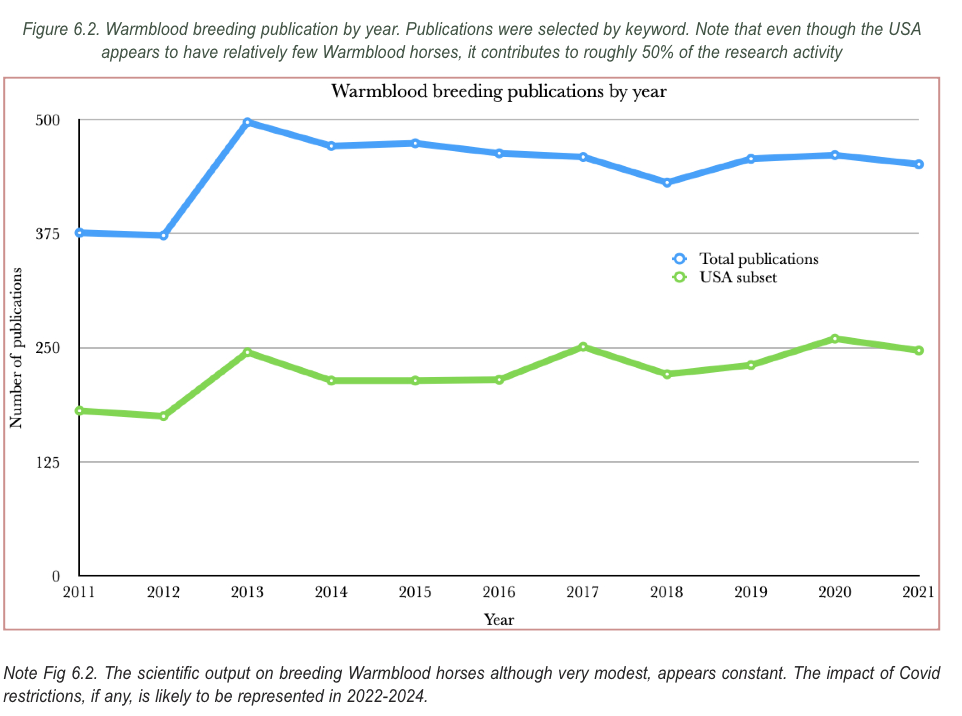

9. Research

Livestock research tends to be concentrated in specialized institutes and land based Universities. A survey of Warmblood breeding research publications supports the notion. There are about 470 breeding papers published each year (Fig 6.2); about seventy of these papers are published by an overlapping group of co-authors, suggesting that the research is broadly collaborative. About half the research is performed in part or in whole in the USA, such that relatively few sites are responsible for the bulk of the publications. These observations make sense. Breeding research will require ethics approval and the ethics boards will require the participation of veterinarians or other specialized investigators. These specialists are located at those Universities that have an adequate land bases and professional Faculties. In the USA these are typically the land-grant institutions and in Europe the national agricultural institutes. Given this narrow base it is not surprising that most publication emanate from relatively few researchers.

10. Issues

10a. Social License

The concept of social license has become an important issue and has a significant impact on the sport horse industry. Activities that are relatively specialized or that have relatively narrow participation are increasingly subject to scrutiny and censure by the society at large. Fortunately horses have a demonstrated broad appeal in the general population, however that innate love of horses means that how horses are treated and used is carefully monitored.

10b. Horse Welfare

Most countries maintain either legislated or voluntary codes of practice. In most cases these codes are based on minimum standards of care and treatment and are an important way that the industry can demonstrate it meets the standards necessary to maintain its social license. There are two issues however. Standards shift over time and may result in impediments to the producer and user of sport horses. Non compliance by individuals are often widely publicized and negatively reflect on the industry as a whole. A number of agencies and organizations are active in the area of animal welfare and in particular horse welfare.

10c. Animal Rights

The animal rights movement is generally considered antithetical to the horse industry. Its arguments and activities often overlap with animal welfare concerns, but are fundamentally different. Within the industry maintaining a high standard of horse welfare is seen as the best way to minimize the migration of public support for rights based opposition to horse activities.

10d. Climate Change

The sport horse industry has been largely oblivious to the potential disruption that climate change could cause to our industry. The issues include: Transportation effects of flying and trucking horses across countries and around the world; feed production effects; loss of land for food for human consumption

10e. Social Benefits

Mitigating some of the negative issues around social license are the social benefits derived from sport horse activities. These should not be minimized or taken for granted and include: Health and fitness; Spectator enjoyment; Psychological well being

10f. Economic Benefits

Social license may also be achieved through demonstrated economic benefits. Comprehensive analysis of the global impact of the industry is currently not possible. A number of national and regional studies have been done that show many positive economic indicators including: High employment sector within agriculture; high spin off economic activity.

11. Comments and Conclusions

During data collection it was clear that organizations that managed both the use and the production of horses (e.g. AQHA, Weatherby’s,…) were able to provide much better insight into their sector. The researchers found that the situation for Warmbloods is very different. Production is overseen by a wide variety of organizations with no single quality metric. Information collected by those organizations often is held internally. The Warmblood-use market includes sport and recreation. The latter, probably large component, is simply a ‘black box’ with little more than anecdotal information available. Similarly, the sport component is not centrally managed. National and sub-national organizations share oversight with the FEI. These latter organizations also declined to share information. The inevitable conclusion is that sport data will be incomplete or incompatible. Longitudinal studies, important for market comprehension, may have so many uncontrolled variables as to be unreliable.

The information we do have does offer some interesting market insights. The Thoroughbred foal sales information spans many years and includes two significant events. The market downturn in 2008 was accompanied by a sharp drop in foal prices because foal production exceeded demand. Anecdotal information suggests that Warmblood breeders experienced a similar phenomenon.

From 2010 to 2018 prices rose for Thoroughbred foals and again, anecdotal evidence suggests that Warmblood markets also recovered. At present, Warmblood auctions are enjoying good prices and strong sales. Production did not increase greatly for either breed. Thoroughbred yearling gross sales returns dropped in 2020 and, given that Warmblood horses are not typically sold as yearlings, it will be informative to see if a similar drop is noted in the 2023 young horse auction prices.

The idea of an annual report is to identify industry trends. For example, we noted above that the AQHA had undergone a major membership drop. Their rationale was that participants “aged out” of the activity. We wondered if this was the case for Warmblood registries. Of course there are many Warmblood registries each with a unique membership cycle. We do not have verified membership numbers for all our studbooks, however it does appear that there has been a general membership decline since 2015. If this trend continues for the coming years, does it suggest that breeders also are “aging out” of the business. Unfortunately, we have no information on the age or the gender of breeders.

Sport use declined because of lockdowns for Covid-19. Showjumping shed 6,000 riders – a 15% decline; dressage lost 900 riders – representing a 23% decline. Given that jumping riders typically have four horses, the loss of so many riders (they may be back) means that 24,000 Warmblood horses are not needed, at least temporarily.

This inaugural report has highlighted the challenges in fully understanding the direction of the sport-horse breeding industry. We have indications that the market is currently good, but we also recognize that it is impacted by political and economic forces well beyond the horse industry. Future reports should delve more deeply into how organizations must act to attract both young breeders and young riders in order to create a strong future for the industry. Leadership must address the larger forces that potentially create headwinds, these include: social license, climate change and horse welfare.

12. Limitations of the Report

We must comment on the exercise to prepare an annual industry report. The researchers were unfamiliar with the data repositories and considerable time was spent identifying them. Only published data was used so some effort was required to transpose the data into a useful presentation. The exercise did build some expertise so that future editions will be more efficiently compiled.

It is important to emphasize the limitations of the data, so we provide some more detailed comments here. The foal registration data was obtained from the WBFSH member-registration information where studbooks self-report the foals registered each year. It is also worth noting that all but two breed associations declined to participate in a survey designed to collect the horse and member demographic details.

The sport data were obtained through the FEI. The geographic usage data, and the data on the numbers of riders per discipline were obtained from the FEI website. Although these numbers are not audited, they are inspected during each event by FEI stewards.

13. ACKNOWLEDGMENTS

The WBFSH gratefully acknowledges the support and cooperation of its partners – the FEI and World Breeding News – in the preparation of this report.

This report was prepared by Chris Gould and Edward Kendall, former vice president and director, respectively, of the WBFSH Development Department.

The authors gratefully acknowledge the research assistance of Dr. Ana Filipe and Ms Nadine Brandtner.

{kind=link}